{kind=link}

By Valerie Velikaya

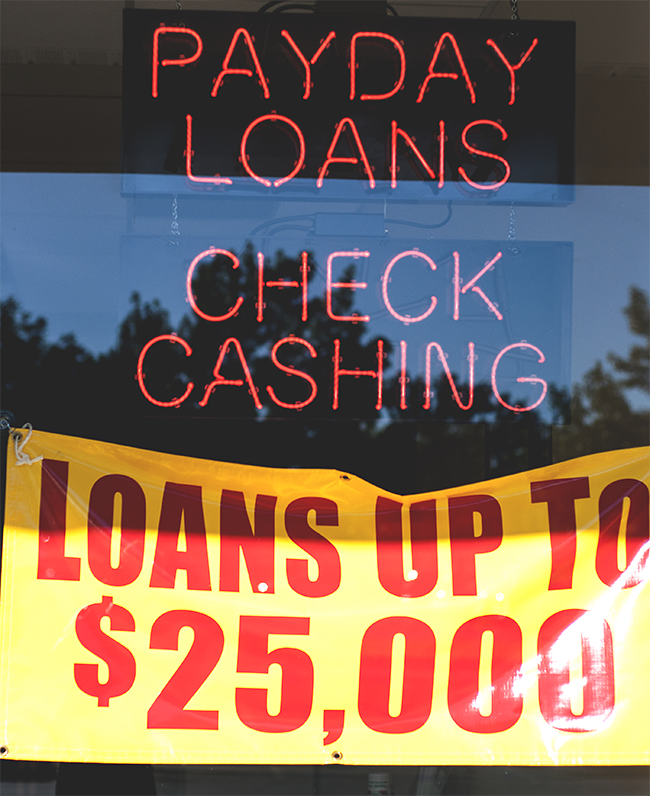

Payday loans are notorious for their high interest rates, loan fees and additional credit expenses; however, they are sugarcoated with evergreen terms such as “cash advance,” “quick cash,” and “cash in 24 hours.”

But deferred deposit loans come at a steep price. Although interest rates depend on the payday lender, short-term loans, regardless of what business, are always due by the customer’s next payday. If the borrower can’t pay the money back during that time period, so begins the cycle of debt and payday loan dependency.

And whether it is Quik Cash or Cash Advance, these short-term loans, generally budgeted at a few hundred dollars, always come with a financing charge.

Nathalie Solger, a third-year student at UMKC who is working on a Bachelor of Science degree in accounting, said that she wishes the payday loan industry would “cease to exist.”

“If you’ve seen any commercials by a payday loan company, you’ve seen that they all appear to be aimed towards people who are having difficulty making ends meet financially,” she said. “In these commercials, payday loan companies send a message that it is simple, easy and not very costly to borrow money.”

Solger said that the payday loan industry targets individuals who are in financial need.

“To financially insecure people, this message can be very appealing because they are often looking for financial help to make ends meet. Well, it may be simple and easy to borrow money from a payday loan company, [but] many people do not realize that it can actually be incredibly costly as well, and unfortunately, it seems that in the payday loan industry there are all too often too many situations in which customers are not properly informed on the actual risks and costs involved in taking out short-term loans.”

Christina Valerio, manager of Check Into Cash in Overland Park, rejects the notion that these loans are schemes. “A lot of times people borrow from us because our fees are less than most,” she said. “It just depends on the situation.”

Valerio said that her business researches their customers’ financial background before a loan is given.

“We’re not going to pay you a $500 loan if we know you can’t pay it back.”

Initially, when looking at a payday loan of $500 with a financing charge of $12 per a hundred dollars, it may not seem like a bad investment as the financing charge would only result in a $60 credit, which develops into a 12 percent rate. In turn, this 12 percent rate is only a simple amount over the course of a two-week period, and it doesn’t represent the complete cost of borrowing, Solger said.

Under the Truth in Lending Act (TILA), federal law requires the official cost of borrowing to be shown through an annual percentage rate (APR), which is calculated based on an annual period.

“So on a $500 loan, the actual cost of borrowing or APR,” said Solger, “is not 12 percent but rather 312 percent. If someone was not able to pay back the $500 two-week payday loan for a year, with an APR of 312 percent, they would end up having to pay back $2,060; $1,560 in fees, plus the original amount of the loan.”

“You have to think of it as you can only borrow what you can pay back,” said Valerio. “You don’t want to get into the routine where you’re borrowing and you can’t pay back. If you’re smart, you’ll take out a loan and then you’ll pay it back.”

Director of Financial Aid Christal Williams cautions individuals seeking to borrow money from payday loan industries. “I would definitely tell them to be careful because the interest on those are very high… extremely high,” said Williams. “I would advise against it. You know, some people it’s a last resort and if it’s a desperate, desperate last resort and you know that on next payday, ‘I can pay this off then I’ll never have to do it again’ – it’s a one time thing, and that’s the only option you have, I’ve seen people do that.

Williams said that her best advice is to weigh out all options. “I mean, there’s Catholic charities. There’s various companies in United Way that will help students pay – help them with expenses if they’re in a bind as opposed to going to that payday loan route.”

Contact Valerie Velikaya, managing editor, vvelikay@jccc.edu